The Healthcare System We Love to Hate

🗓️ 2024-12-07

The news this week has brought a storm of emotions back from the depths for me. I feel obligated to say something, having worked in the health (and long-term care, or LTC) insurance industries for a combined seven years as an actuary.

A quick aside if you don't know what an actuary is or does: at the core, they are tasked with making sure that their insurance company (or client, or government) collects enough money on one side to pay claims on the other side. There are variants on this ultimate goal and side quests depending on where they work, but every insurance company you know has at least one (and probably a bunch).

This is not a glorification of the murder of a major health insurer’s CEO. That story deserves its own analysis. As a former insider, my goal here is to help explain why the general public feels so burdened and taken advantage of by our health insurance system that many seem almost celebratory with the news. (It matters little, but my personal, raw emotional reaction to the breaking story on Wednesday morning was a total lack of surprise.)

An insurance primer

I strongly believe that insurance is a public force for good. In fact, we know that the core idea is popular because humanity has looked for ways to de-risk their lives since the dawn of civilization. It’s hard to think of a concept that delivers much more of a community benefit (maybe third places? food banks?). The fundamental concept of insurance is this:

- individuals come together to form a group (pretend you’re included in this group, because you probably are)

- you and each individual promises that if one person in the group has an unlucky year (house burns down, cancer diagnosis, other catastrophic life event), you and the others will split the cost of this event

- in exchange for this promise, the group will return the favor and cover your costs if you’re the one that experiences the loss, which will prevent your quality of life from being destroyed by misfortune

Seems pretty useful, right? And the bigger the group, the more we can spread the risk around. One unlucky event for a group of two people would still be pretty bad financially for both people…but one unlucky event for a group of 200 people seems much more manageable.

The problem is not the concept of insurance. The problem is for-profit health insurance.

The duty of an actuary

I believe that those continuing down the path of health actuary in the United States have a duty to help the general public understand the relationship between:

- the incentives of U.S. for-profit health insurance companies, and

- the needs of the general population that are seeking care

Through my analysis and studying the analysis of others, the conclusion I kept arriving at was that there is no way for these two forces to meet-in-the-middle and compromise. Profit-seeking insurance companies will continue to look for ways to maximize profits. This will ever be at odds with public health, because health care costs money. Anyone can see that the insurance company wins when a claim is denied (and many have experienced these denials first-hand).

After much internal struggle a few years ago, I quit the insurance industry and the entire actuarial profession because of this conclusion. But as a former actuary, I still hold myself to the duty of communication. We are the world’s experts on insurance. Of course I will continue to answer my friends’ open enrollment questions and help Grandma understand her Medigap options…but in my eyes, this is no longer enough.

No matter who I work for, I am still beholden to the industry like most of the public, thanks to the concept of employer-sponsored health insurance. What started as a way for employers to compete for talent without raising wages has dodged reform after reform, instead growing into a ball-and-chain that keeps us all on the corporate treadmill for fear of what would happen to our financial security if we ever had a ruinous diagnosis. (Cancer claims, life-altering burns, and nursing home costs all have the capability to wipe out life savings without insurance protection, to name just a few.)

The most generous, most affordable plans you can find are the ones provided by the relatively generous employers. You must work for one of these employers to participate in these plans, and the reason the plan might be affordable to you is that your employer will usually pay the lion’s share of the cost of coverage. If you ever change jobs, your employer likely won’t be helping out anymore, so you’re stuck paying full-cost (102%, actually) COBRA rates until your new coverage kicks in. (I would wager that this is when most people find out that yes, individual health coverage actually costs almost $1,000 a month and your employer was paying most of it, but now you have to. Need family coverage? Brace yourself.)

If you can’t afford to cling to your old employer’s COBRA coverage while between jobs, you’re stuck looking for individual coverage. Good luck. Obamacare (the Affordable Care Act) made finding individual coverage easier, but it definitely still didn’t make it easy.

If you want to work for yourself and/or start a business, you’re stuck looking for individual coverage. Good luck.

As a health actuary, I was 100% guilty of disassociating:

“I’m not the one denying claims; that’s the claims department. I just analyze.”

Or:

“I’m not the one deciding to cut employee benefits; that’s the client. I just implement.”

But despite this form of coping, the revenue from such activities was undeniably still resulting in personal profit.

If you still believe that the concept of for-profit health insurance can work, then as part of your duty to communicate, you should also explain why:

- Medicare is the most well-liked health insurer in the U.S.;

- the rest of the world doesn’t do things the U.S. way, spends way less, and has better health outcomes than us; and

- the private health insurers in America are so unpopular that the death of one of its CEOs is being celebrated to the tune of thousands of Facebook laughing emojis and TikTok songs.

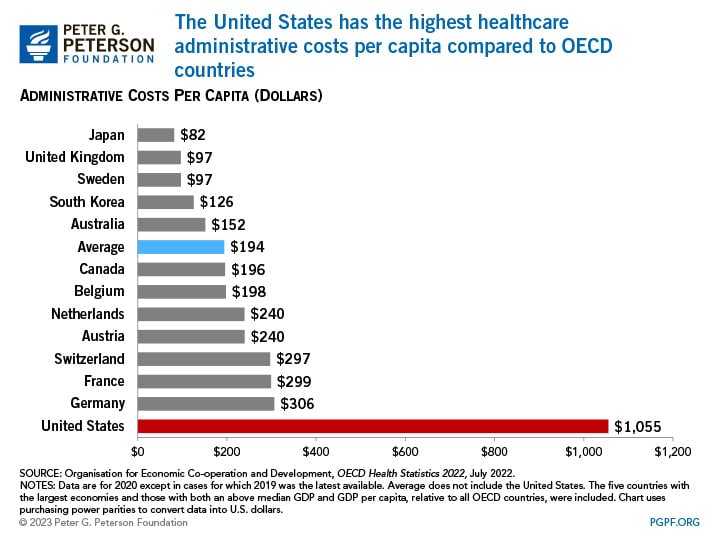

If you believe a concept such as universal healthcare is unachievable in the U.S. because there’s simply not enough to go around, you should question why doctor shortages are getting worse while administrative (non-doctor) costs continue to climb. (This is precisely why my primary care doctor told me last month that he would no longer recommend the medical field that he once had a passion for to anyone, not even to his own children.) It suggests to me that society needs less middlemen in Excel spreadsheets and more doctors. Can we not achieve this?

{kind=link}

Do people truly believe that not everyone should be able to afford or access healthcare? How is this ethical?

Credible arguments in support of the current system are becoming scarce. Any such argument must address the points above, and why the current system lets those who can’t afford coverage to simply go without care and/or die. This is a cruel system by definition, one that I could not stomach working in anymore.

Should I have stayed and tried to be a force for change from the inside? Maybe, but I personally didn’t see a successful path toward doing anything remotely impactful. These companies are systematically built, designed, and optimized to maximize shareholder value, not public health. Public sentiment this week seems to confirm that things have only gotten worse since I left three years ago.

Even if we can’t change things from the inside, we must do something. Clearly, the public is exhausted by the insanity of trying to predict their medical future and “shopping” between the $3,000 deductible PPO plan and the $5,000 deductible HDHP (hooray, open enrollment). Clearly, the public has grown fully tired of the claims roulette rejecting their medically-necessary procedure, sometimes even hours before a surgery. And clearly, the public (rightly) does not buy that this is the best we can do as a society.

But it is not enough for me to stand before you tonight and condemn riots. It would be morally irresponsible for me to do that without, at the same time, condemning the contingent, intolerable conditions that exist in our society. These conditions are the things that cause individuals to feel that they have no other alternative than to engage in violent rebellions to get attention.

I think our great hope lies in the fact that the vast majority of folks in the U.S. despise the current system, and know it’s working against them. We’ve been reminded of this in the darkest way this week, yet we are reminded all the same. Healthcare for all, without a profit motive, is a popular idea. We owe it to ourselves and our communities to fight for it. ⚪️

Resources

Back in August 2021 as I was on the brink of quitting actuarial, I vented my frustration by writing myself a long rant that I called The Tired Actuary. Over the past three years, multiple individuals in the industry have reached out after seeing my career transition, wondering how they can replicate it…and almost always in my conversations with them, I hear the same themes that I wrote to myself back then. Folks are tired of strengthening pillars of oppressive systems, tired of being billable hour machines, and tired of pushing numbers around in spreadsheets. In a word: burnout.

Burnout clearly played a leading role in my decision to exit the health insurance industry and actuarial profession — I happen to be working my way through Burnout Immunity by Kandi Wiens, EdD right now, and I wish I’d had the book three years ago when writing The Tired Actuary. Turns out it’s proven through research that a mismatch between your values and your company/industry’s values is a huge contributing factor to burnout (among other things), and when you find purpose in your work, you build up an immunity to burnout.

No matter what you do for work, I would highly recommend the book if you’re feeling numb or lost on the job lately. (If you’re a podcast person, her recent appearance on Alie Ward’s Ologies is what originally resonated with me, which led me to the book.)

Other thoughts

This is a side issue to the main focus of the article, but we should also ask ourselves why we pay more when we have to make a repeat visit to the doctor, for the same reason we’re upset when we take our car into the shop once, it breaks in a few days, and we have to take it to the shop again. Why are we paying twice for the same repair (especially if the issue is easily diagnosed and managed)? The long story short is that:

- We would need a paradigm shift toward paying doctors based on outcomes instead of per-service…

- And while we’re stuck with a fee-for-service (FFS) payment model, system forces continue to push for less doctor-patient time so that more patients/admin tasks can be squeezed in for more $$$, which is increasing doctor burnout and reducing care quality.

Oh, and one more thing: private equity is destroying hospitals.